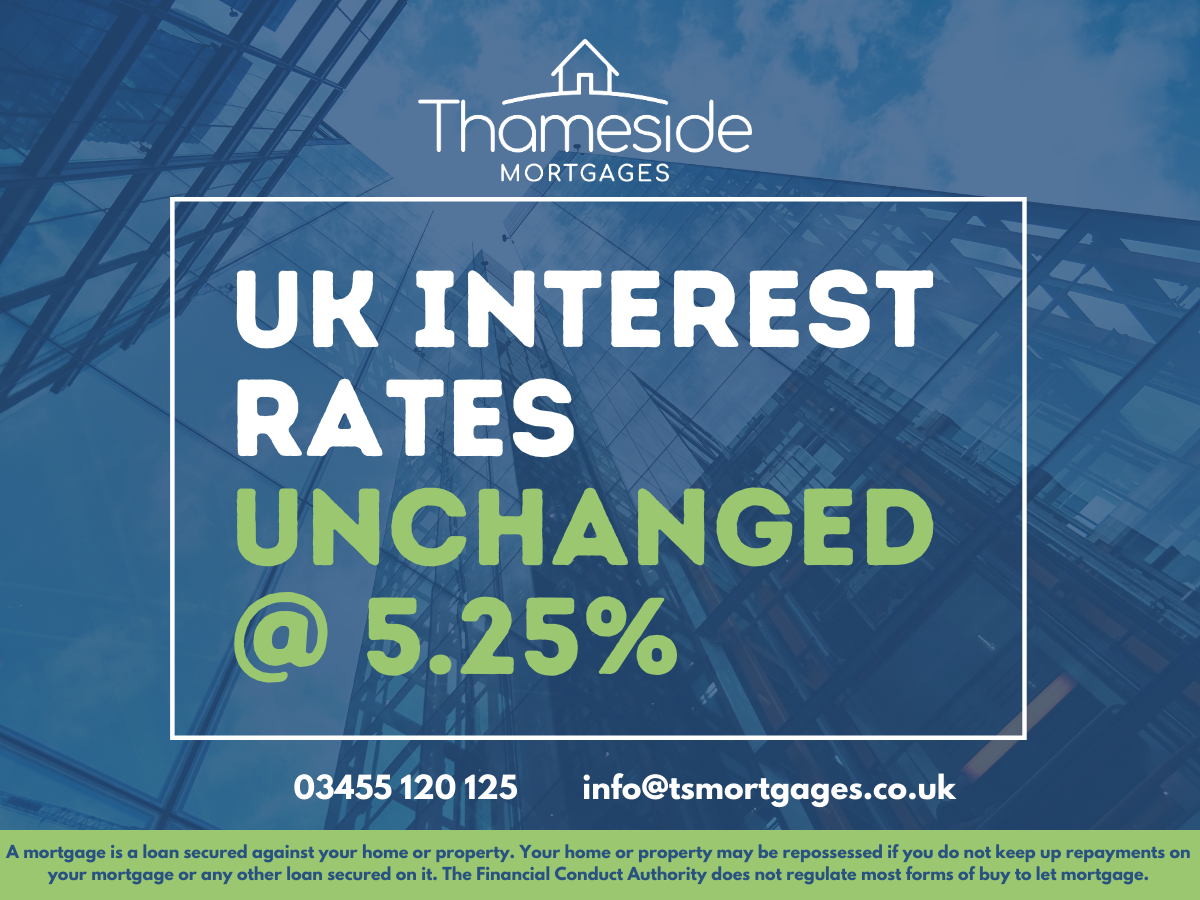

The Bank of England have voted to raise the UK interest rate from 0.10% to 0.25%, which is likely to have an impact on UK mortgage rates.

The Base Rate has previously been held at a record low 0.10% since the pandemic started in March 2020, but has been increased today amid growing pressures under the high UK inflation rate, caused by a surge in consumer prices, high energy costs and significant labour shortages.

The UK Inflation Rate target is 2.00% but was 3.10% in September and surged by 5.1% in the 12 months to November.

“It seems mortgage lenders were anticipating this rise as we’ve seen a quite a few mainstream mortgage lenders withdraw their sub-1.00% mortgage deals in the last few weeks“.

Andrew Sheen, Managing Director.

Does Rising Inflation Need To Be Dealt With?

The Monetary Policy Committee (MPC) is tasked with ensuring inflation does not rise above 2.00%. If Inflation rises above 3.00% (or as low as 1.00%), the Governor of the Bank of England, Andrew Bailey, has to write to the Chancellor, Rishi Sunak to explain what he’s going to do about it.

Raising UK interest rates is a difficult decision to make. If they increase too much, it can stop the economic recovery and even cause a recession. The Bank of England hesitated to raise rates prior to today, in the hope that the rising inflation was short lived.

A number of factors have led to the rise of inflation, such as shortages in raw materials, increased consumer demand, lack of labour/workforce (including logistics/transportation).

While inflation was almost zero at the beginning of 2020, it rose sharply to 3.20% in August, before falling back to 3.10% in September.

The main reason behind increasing interest rates is to make it more expensive to borrow money – great for savers, but not for borrowers.

What does this mean for UK mortgage rates?

We’ve already seen the sub-1.00% mortgage deals disappear over the last few weeks. According to Defaqto, there were 82 sub-1.00% mortgages available, but as of 2nd November, that number dropped significantly to just 22.

However, there is still time to secure a great deal as Interest rates are still significantly lower compared with previous years.

If you have a fixed rate mortgage, you can still secure a new deal with 6 months remaining on your fixed rate. While your existing lender is not likely to offer you a new deal until there are 2-4 months left, we can secure a deal ready for when your fixed rate expires.

We strongly believe that obtaining professional advice is key to finding the right deal for you, so why not reach out to see how we can help.

You can call us on 03455 120 125, email us at info@tsmortgages.co.uk or live chat with one of our team.

www.tsmortgages.co.uk

Post from Thameside Mortgages

A mortgage is a loan secured against your home or property. Your home or property may be repossessed if you do not keep up repayments on your mortgage or any other loan secured on it. The Financial Conduct Authority does not regulate most forms of buy to let mortgage.