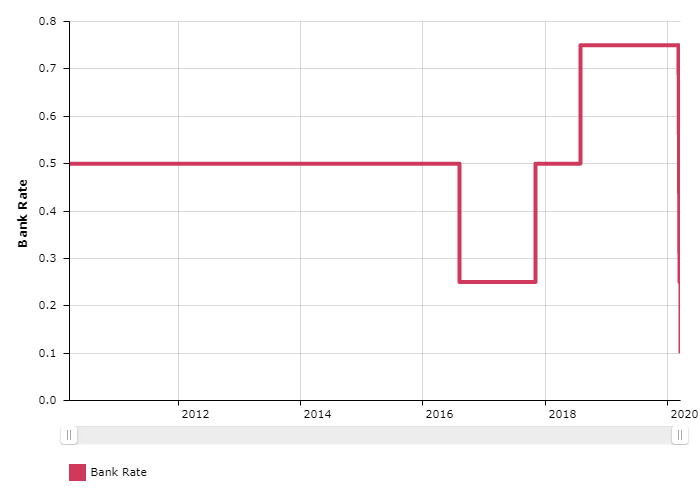

The Bank of England has risen interest rates for a 13th consecutive time as it continues to tackle rising prices.

Experts were predicting a slight fall in inflation figures in May, but official data on Wednesday showed inflation was still stuck at 8.7% in May, due to increased prices for second-hand cars, flights and supermarket food prices.

The Base Rate of 5.00% is the highest the UK has seen since 2008.

Just one month ago experts were predicting we were nearing the end of rate rises, but the rhetoric has changed as base rate could now reach 6.00% – a figure not seen since the 1990’s.

Thameside Mortgages Managing Director, Andrew Sheen pointed out “a fundamental role of the Bank of England is to control inflation. It’s painfully obvious increasing rates has been an ineffective tool against inflation.

“Rather than stubbornly sticking to the same methods, they should take a moment to pause and consider a different approach before causing significant harm to the economy and people’s livelihoods.”

The Bank of England announced it has increased interest rates once again, to 4.50%, marking the 12th consecutive increase in rates from the Bank of England.

This article emphasises the importance of early mortgage review and explores the potential effects of rising interest rates.

Becoming a homeowner is a dream for many renters, but the hefty deposit requirements can often make it seem impossible. With house prices and the cost of living on the rise, saving five-figure sums for a deposit can be a daunting prospect. But now, there is a solution.

6 common mistakes to avoid before trying to purchase a property

Buying a home for the first time can be an exciting and intimidating experience. It’s important to approach the process with caution and avoid common mistakes that can cost you time, money, and headaches. In this blog article, we will discuss the 6 most common mistakes that first-time homebuyers make and provide tips on how to avoid them.

Whether you’re in the market for a new home or just starting to think about buying, this article will help you navigate the process with confidence and ease. So sit back, relax, and get ready to learn how to avoid the most common pitfalls of first-time homebuyers.

If you have any questions or concerns about the home-buying process, don’t hesitate to reach out to us. We are here to help you make informed decisions and guide you through every step of the way.

You can contact us via 03455 120 125, use our contact form, or you can even use our online chat feature. We are happy to hear from you and provide any assistance you need.

Failing to establish how much you can borrow

Before you start viewing properties, you should establish how much you’re able to borrow. Once you’ve worked this out, you will have an accurate price range and begin to view properties.

Not working out a monthly budget you can afford

There’s no point buying a house if you cannot afford to leave it. Knowing how much you can borrow will help you understand how much your mortgage payments are likely to be, so you can budget accordingly.

Not having the correct documents ready

To accurately work out your affordability, you should ensure you have payslips/tax returns and your credit report to hand. Without these documents, no adviser will be able to provide accurate figures and things become guesswork. There’s nothing worse than viewing a property you love, then realising you cannot afford it. Your adviser will confirm exactly what you’ll need.

Not getting an AIP, or Agreement in Principle

When you make an offer on a property, an estate agent will ask for your Agreement in Principle – a piece of paper that confirms a mortgage lender has provisionally approved the amount you would like to borrow. If you don’t have this in place, they may not take your offer seriously and move onto another buyer.

Choosing a solicitor based on cost

It can take more than three months to complete a purchase – it’s the legal work that takes the greatest amount of time. There are lots of solicitors that may appear extremely cheap, but they can be very slow to respond, update or communicate, which adds a significant amount of time and stress.

Sometimes, if you can pay a little bit more and obtain a solicitor who will be proactive, experienced, great with chasing the other side and will communicate their updates with you. Choosing the right solicitor can remove a lot of stress.

Choosing the wrong mortgage broker

Choosing the right mortgage broker is crucial. Read reviews from previous clients to ensure they are the right fit for you. They should help you understand the pros and cons of each option. A good broker will update the estate agent on your behalf, liaise with the solicitor for progress reports and keep you updated each step of the way. They will discuss the importance of life assurance, home insurance and any other relevant insurances and discuss the importance of writing a Will.

Essentially, the right adviser will guide you from the start, through to the finish – and beyond.

We’ve covered some of the common mistakes that first-time homebuyers should avoid, but there may be others that we haven’t mentioned. If you want to learn more about how to avoid these pitfalls and make informed decisions, please don’t hesitate to contact us.

At Thameside Mortgages, we have a dedicated team of professionals who are happy to help you navigate the home-buying process. You can reach us by phone at 03455 120 125, use our contact form on our website, or via our online chat feature.

We look forward to hearing from you and helping you achieve your homeownership goals!

The Bank of England recently announced that it had increased interest rates to 4.25%.

In this article, we highlight the significance of reviewing your mortgage as early as possible and delve into the consequences of increasing interest rates.

The Bank of England have voted to raise the UK interest rate from 0.10% to 0.25%, which is likely to have an impact on UK mortgage rates.

The Base Rate has previously been held at a record low 0.10% since the pandemic started in March 2020, but has been increased today amid growing pressures under the high UK inflation rate, caused by a surge in consumer prices, high energy costs and significant labour shortages.

The UK Inflation Rate target is 2.00% but was 3.10% in September and surged by 5.1% in the 12 months to November.

“It seems mortgage lenders were anticipating this rise as we’ve seen a quite a few mainstream mortgage lenders withdraw their sub-1.00% mortgage deals in the last few weeks“.

Andrew Sheen, Managing Director.

Does Rising Inflation Need To Be Dealt With?

The Monetary Policy Committee (MPC) is tasked with ensuring inflation does not rise above 2.00%. If Inflation rises above 3.00% (or as low as 1.00%), the Governor of the Bank of England, Andrew Bailey, has to write to the Chancellor, Rishi Sunak to explain what he’s going to do about it.

Raising UK interest rates is a difficult decision to make. If they increase too much, it can stop the economic recovery and even cause a recession. The Bank of England hesitated to raise rates prior to today, in the hope that the rising inflation was short lived.

A number of factors have led to the rise of inflation, such as shortages in raw materials, increased consumer demand, lack of labour/workforce (including logistics/transportation).

While inflation was almost zero at the beginning of 2020, it rose sharply to 3.20% in August, before falling back to 3.10% in September.

The main reason behind increasing interest rates is to make it more expensive to borrow money – great for savers, but not for borrowers.

What does this mean for UK mortgage rates?

We’ve already seen the sub-1.00% mortgage deals disappear over the last few weeks. According to Defaqto, there were 82 sub-1.00% mortgages available, but as of 2nd November, that number dropped significantly to just 22.

However, there is still time to secure a great deal as Interest rates are still significantly lower compared with previous years.

If you have a fixed rate mortgage, you can still secure a new deal with 6 months remaining on your fixed rate. While your existing lender is not likely to offer you a new deal until there are 2-4 months left, we can secure a deal ready for when your fixed rate expires.

We strongly believe that obtaining professional advice is key to finding the right deal for you, so why not reach out to see how we can help.

You can call us on 03455 120 125, email us at info@tsmortgages.co.uk or live chat with one of our team.

A mortgage is a loan secured against your home or property. Your home or property may be repossessed if you do not keep up repayments on your mortgage or any other loan secured on it. The Financial Conduct Authority does not regulate most forms of buy to let mortgage.

On 31st March 2020, we read an article from the BBC titled ‘UK mortgage market goes into lockdown’, which stated that “Nationwide, one of the UK’s biggest lenders…has effectively pulled out of new lending, only offering mortgages to those who have 25% deposit/equity or more….which rules out First Time Buyers”.

We felt this article creates the very panic everyone in my industry is trying to avoid and leaves people wondering if this is due to Nationwide predicting a huge slump in house prices.

While we cannot guess what will happen with UK property market, we can explain the reasons why mortgage lending is becoming more restrictive directly as a result of the lockdown.

The Bank of England has once again cut interest rates in an emergency move to shore up the UK economy in the wake of the Covid-19 pandemic.

This is the lowest interest rate in the history of the Bank of England.

The Bank is also looking to restart its Quantitative Easing measures, by increasing its holdings of bonds by£200bn.

It was just last week that the Bank of England moved to reduce rates to 0.25%

Get In Touch – Live Chat

We have already been speaking with our own customers about this, but we have also spoken with new clients who would like to revisit their finances and compare their current mortgage rates to the already extremely low rates on offer from the 90+ mortgage lenders we have access to.

We have a Live Chat facility on our website that can help answer your questions.

Your home may be repossessed if you do not keep up repayments on your mortgage. There may be a fee for mortgage advice. The actual amount you pay will depend upon your circumstances, a typical fee will be £399

On 11th March, the Governor of the Bank of England, Mark Carney announced that interest rates would be reduced to 0.25% in order to support businesses and consumer confidence during a time of crisis.

Less than a week later, Chancellor Rishi Sunak unveiled £330bn of extra support to help businesses and individuals deal with the financial difficulties that are being caused by the Covid-19 outbreak.

These two decisions highlight the Chancellor’s comments during a news conference, that a “collective national effort” would be required to get us through this.

On Wednesday 11th March 2020, the UK Bank of England announced that they have reduced interest rates by 0.50%, to 0.25% as a response to the wake of the Coronavirus.

We have already received an unprecedented amount of enquiries from new and existing clients asking what this may mean for them.